Private Credit Interview Guide

Private credit interviews test whether you think like a lender. This is how you get there.

80 questions with model answers, case-study drills, cheat sheets, and a deal memo framework — one prep stack built around how direct lenders actually interview.

$197 · Instant digital download · Direct lending / special situations / private debt

Our students got offers from

The real problem

Why most candidates still sound generic in the room

They prepare like it's a private equity interview. They can talk about the company, but not the credit. They know leverage matters, but not where the risk really sits when docs tighten or the downside gets ugly.

What's inside

The complete prep stack. Four components.

Specific enough to sound lender-first. Tight enough to stay useful the week of the interview.

80 Q&A + model answers

Questions built for how lenders actually interview

Covers leverage, downside, free cash flow conversion, covenant packages, documentation traps, sponsor behavior, and structure — with model answers that show lender-first thinking, not textbook definitions.

Case-study drills

The formats where most candidates lose control

Three formats built around the hardest interview moments: framing risk under pressure, identifying the real swing factor, and landing a credit recommendation. With worked examples.

Cheat sheets

Fast-review pages for the week of the interview

Maintenance vs incurrence covenants, headroom, leakage, documentation red flags, deal structure, and the points interviewers use to separate real credit judgment from polished buzzwords.

Deal memo framework

Turn a messy case into a structured investment view

A repeatable approach to walking through business quality, leverage, downside, documentation, and recommendation — in the format a direct lender recognizes.

Open the guide

This is what a real answer looks like.

Not summaries. Not bullet lists. Model answers that show the lender logic behind the question.

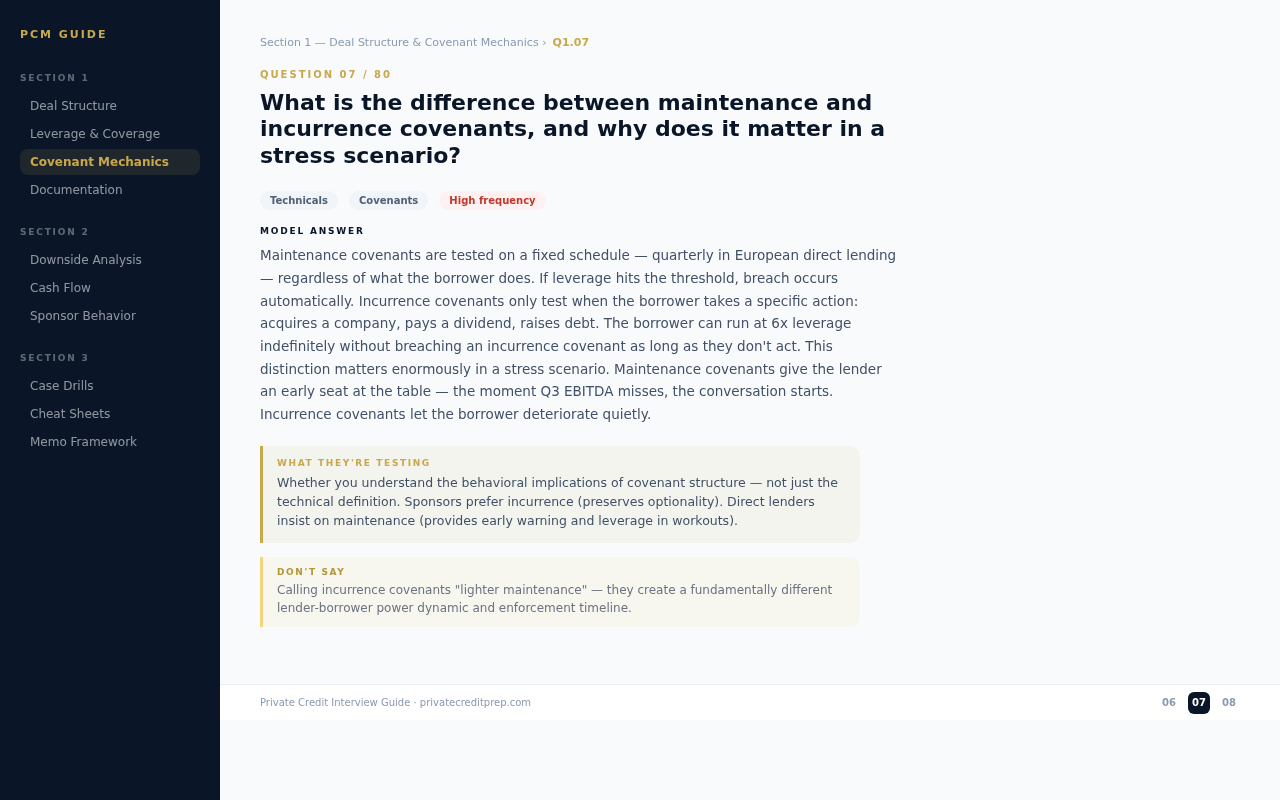

What is the difference between maintenance and incurrence covenants?

Maintenance covenants are tested on a fixed schedule — quarterly in European direct lending — regardless of what the borrower does. If leverage hits the threshold, breach occurs automatically. Incurrence covenants only test when the borrower takes a specific action: acquires a company, pays a dividend, raises debt. The borrower can run at 6x leverage indefinitely without breaching an incurrence covenant as long as they don't act. This distinction matters enormously in a stress scenario. Maintenance covenants give the lender an early seat at the table — the moment Q3 EBITDA misses, the conversation starts. Incurrence covenants let the borrower deteriorate quietly. That's why sponsors prefer incurrence (preserves optionality) and direct lenders insist on maintenance (provides early warning and leverage in workouts).

The behavioral and enforcement implications of covenant structure. Asked at Lazard, SG MidCap, and Rothschild.

Calling incurrence covenants “lighter maintenance” — they create a fundamentally different lender-borrower power dynamic.

- Working capital is the cash tied up in day-to-day operations before it reaches the lender.

- An increase in receivables means the company booked revenue but has not collected cash.

- Negative working capital is only good if it is structural and durable through a downside.

- Two companies can report the same EBITDA and have very different debt capacity if one converts cash and the other traps it.

Company: €120M revenue, €20M EBITDA. DSO at 45 days → receivables ≈ €14.8M. DSO deteriorates to 60 days → receivables ≈ €19.7M. Cash trapped: ~€4.9M — 25% of EBITDA consumed by working capital alone, before CapEx, taxes, or interest.

A 15-day DSO deterioration on €120M of revenue traps roughly €5M of cash. On a €20M EBITDA business, that is a quarter of your earnings stuck in receivables.

There are 79 more Q&As and 9 more cheat sheets like this in the guide.

Interior page from the guide — Section 1, Question 7 of 80

Most prep content treats private credit like a lighter version of private equity. That is exactly why candidates sound generic.

This guide is built around how lenders actually think: downside first, documentation matters, structure matters, and a good company is not automatically a good credit.

FAQ

Common questions before checkout.

Who is this for?

Candidates targeting private credit, direct lending, special situations, or broader private debt roles — especially analysts and associates preparing for interview loops where lender judgment matters more than modeling polish.

Who isn't it for?

It's not a modeling course, a general finance primer, or motivational material. It assumes you can already read a P&L and understand basic leverage. The value is in answering with sharper lender-style framing.

Is this a generic finance course?

No. The value is in private-credit-specific interview framing: downside, docs, structure, covenants, and the exact credit logic candidates usually miss when they prep with broad finance material.

How do I get access?

Instantly after purchase. You receive the guide digitally and can work through it in sequence or use it selectively the week of your interview.

Digital PDF · Instant download after purchase · 4 PDFs in the pack

Questions about your order? support@privatecreditprep.com

$197

Stop sounding like a PE candidate in a credit interview.

80 questions, real case formats, cheat sheets, and a deal memo framework — built for how private credit lenders actually run interviews. Instant download.